It wasn’t so much ‘Mad March’ as ‘Meagre March’ for the car industry, with retail new car sales showing little growth and electric car sales flatlining.

March is traditionally the biggest month of the year for new car sales, so its results tend to be of great significance for the industry. And based on the results published this morning by the Society of Motor Manufacturers and Traders (SMMT), things are looking lukewarm at best.

Private new car sales showed little growth, with a 1% increase over the same month last year. Fleet registrations were up 41% as the sector continued its rebound from historic lows last year, meaning that overall registrations were up 26% compared to last March.

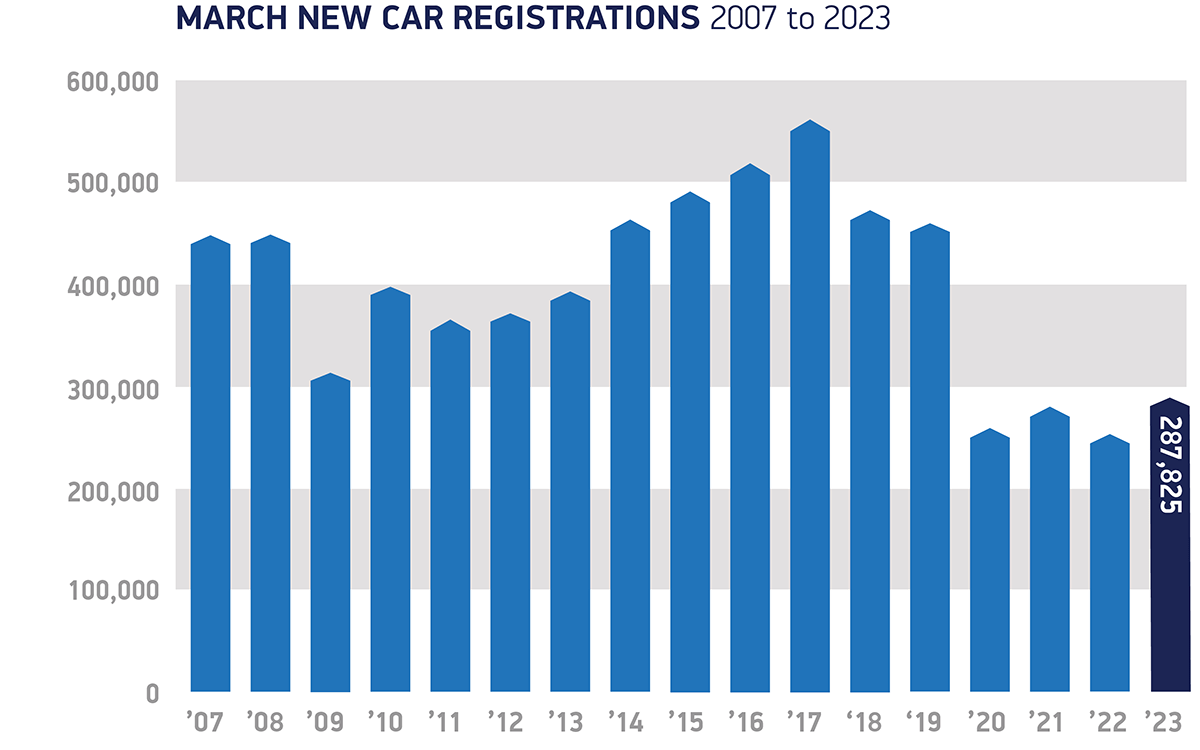

While the SMMT hailed the results as “the best ‘new plate month’ performance since before the pandemic”, it was still down nearly 40% on the numbers from March 2019 and 2018. The chart below of March results from 2007 to 2023 show the scale of the impact of the Covid pandemic and its after-effects on the industry, which are still clearly being felt today.

Fleet bounceback masks flat retail sector

The headline growth in the sales numbers is entirely the result of rebounding fleet sales, which were far more depressed than retail sales over the last three years. As such, what looks like an impressive growth figure is actually a rebound from a terrible performance last March.

Almost exactly 140,000 new cars were registered to fleets in March, which was a strong growth over last year, when that number was only about 99,000. But go back a year further to 2021, and it was 151,000. Pre-pandemic, we would expect to see 220,000+ registrations in March. So it was improvement, but not really enough to break out the party hats.

For private new car sales, it was very flat with results that were little better than last year, and again a long way down on pre-Covid numbers. The well-documented cost-of-living crisis, coupled with increasing interest rates that are making cars ever-more expensive, is presumably having a significant impact on the retail sector.

| Buyer | March 2023 | March 2022 | % change | Market share 2023 | Market share 2022 |

|---|---|---|---|---|---|

| Private | 139,223 | 137,302 | 1.4% | 48.4% | 56.4% |

| Fleet | 140,002 | 99,351 | 40.9% | 48.6% | 40.8% |

| Business | 8,600 | 6,826 | 26.0% | 3.0% | 2.8% |

| Total | 287,825 | 243,479 | 18.2% |

Source: SMMT

EV sales flatlining

Another headache for both car makers and the government – almost certainly connected to cost concerns– will be stagnant sales of electric cars. The market share for EVs was 16%, exactly the same (to within 0.1%) as last March. Plug-in hybrids fared poorly, yet again, falling well short of overall market growth.

The only good news for EV sales was that a larger proportion of sales came from brands other than Tesla, which had a relatively poor month compared to last March. The Model Y did top the sales charts again and outperformed the overall market, but the Model 3 saloon sold in far fewer numbers than the same month last year.

[Tesla tends to concentrate its registrations into selected months of the year rather than delivering a steady stream of new cars every month. As the largest electric car manufacturer operating in the UK, this has a boom/bust effect on EV market share, so we tend to look at quarterly data more closely than monthly results.]

The government is planning to introduce a mandate to force car makers to sell a minimum percentage of EVs starting from next year. But unless it can find ways to encourage people to choose an electric car, all this will achieve is to reduce overall new car sales.

New car registrations by fuel type

| Fuel | March 2023 | March 2022 | % change | Market share 2023 | Market share 2022 |

|---|---|---|---|---|---|

| Petrol* | 162,046 | 135,065 | 20.0% | 56.3% | 55.6% |

| Electric | 46,626 | 39,315 | 18.6% | 16.2% | 16.1% |

| Hybrid | 37,252 | 27,737 | 34.3% | 12.9% | 11.4% |

| Diesel* | 23,968 | 25,325 | -5.4% | 8.3% | 10.4% |

| Plug-in hybrid | 17,933 | 16,037 | 11.8% | 6.2% | 6.6% |

| Total | 287,825 | 243,479 | 18.2% |

*includes mild hybrids

Source: SMMT

Good month, bad month

Within the overall market, there are always some brands that are performing well while others lag behind. With March being such a big month for the car industry, the results provide key insight into which brands are flying and which are floundering.

It was a good month for Cupra, Dacia, Genesis, Honda, Jeep, Land Rover, Maserati, Mazda, MG, Mini, Nissan, Polestar, Porsche, SEAT, Skoda, Subaru and Volkswagen. All of these brands overperformed against the overall market by at least 10%.

Meanwhile, life wasn’t so rosy for Abarth, Alfa Romeo, Alpine, Bentley, BMW, Fiat, Jaguar, Lexus, Peugeot, Renault, Smart, SsangYong, Tesla, Vauxhall and Volvo. All of these brands underperformed against the overall market by at least 10%.

That means that the following brands were all more or less in line with overall market growth: Audi, Citroën, DS Automobiles, Ford, Hyundai, Kia, Mercedes-Benz, Suzuki and Toyota.

Volkswagen continues to be the UK’s best-selling car brand, – despite not having a single car in the top ten for March – ahead of Ford. Audi is holding off Kia for third place, while Nissan has jumped from tenth to sixth off the back of its strong March performance for its two British-built crossovers.

March

| Rank | Brand | Registrations | Market share |

|---|---|---|---|

| 1 | Volkswagen | 21,747 | 7.6% |

| 2 | Ford | 20,415 | 7.1% |

| 3 | Kia | 19,703 | 6.9% |

| 4 | Toyota | 19,253 | 6.7% |

| 5 | Audi | 19,039 | 6.6% |

| 6 | Nissan | 16,994 | 5.9% |

| 7 | Mercedes-Benz | 16,443 | 5.7% |

| 8 | BMW | 14,463 | 5.0% |

| 9 | Hyundai | 13,532 | 4.7% |

| 10 | MG | 12,232 | 4.3% |

Source: SMMT

Year to date

| Rank | Brand | Registrations | Market share |

|---|---|---|---|

| 1 | Volkswagen | 40,991 | 8.3% |

| 2 | Ford | 36,423 | 7.4% |

| 3 | Audi | 32,698 | 6.6% |

| 4 | Kia | 32,255 | 6.5% |

| 5 | Toyota | 31,748 | 6.4% |

| 6 | Nissan | 25,950 | 5.3% |

| 7 | BMW | 25,846 | 5.2% |

| 8 | Hyundai | 24,087 | 4.9% |

| 9 | Mercedes-Benz | 23,683 | 4.8% |

| 10 | Vauxhall | 22,854 | 4.6% |

Source: SMMT

Model Y back on top

With a very strong sales performance, the Tesla Model Y hit the top of the charts in March. It also becomes the third different car to top the best-sellers list in the three months of this year.

It was another strong result for Nissan in March, with two of its UK-built cars in the top three. The smaller Juke outsold the larger Qashqai in March, but the Qashqai has edged its way to the top in year-to-date sales, just ahead of its smaller sibling.

Small-to-mid-sized crossovers dominated the charts, with seven of the top ten vehicles sold. Three supermini-sized hatchbacks – the Vauxhall Corsa, Mini hatch and Ford Fiesta – made up the rest of the top ten.

We have our full analysis of the best-sellers here.

March

| Rank | Brand | Registrations |

|---|---|---|

| 1 | Tesla Model Y | 8,123 |

| 2 | Nissan Juke | 7,532 |

| 3 | Nissan Qashqai | 6,755 |

| 4 | Kia Sportage | 5,888 |

| 5 | Hyundai Tucson | 5,680 |

| 6 | Ford Puma | 5,652 |

| 7 | Vauxhall Corsa | 5,588 |

| 8 | Mini hatch | 5,401 |

| 9 | Toyota Yaris Cross | 5,214 |

| 10 | Ford Fiesta | 4,792 |

Source: SMMT

Year to date

| Rank | Brand | Registrations |

|---|---|---|

| 1 | Nissan Qashqai | 11,073 |

| 2 | Nissan Juke | 10,875 |

| 3 | Vauxhall Corsa | 10,831 |

| 4 | Tesla Model Y | 9,953 |

| 5 | Kia Sportage | 9,559 |

| 6 | Ford Puma | 9,558 |

| 7 | Hyundai Tucson | 9,467 |

| 8 | Mini hatch | 8,328 |

| 9 | Ford Fiesta | 8,137 |

| 10 | Volkswagen T-Roc | 8,120 |

Source: SMMT