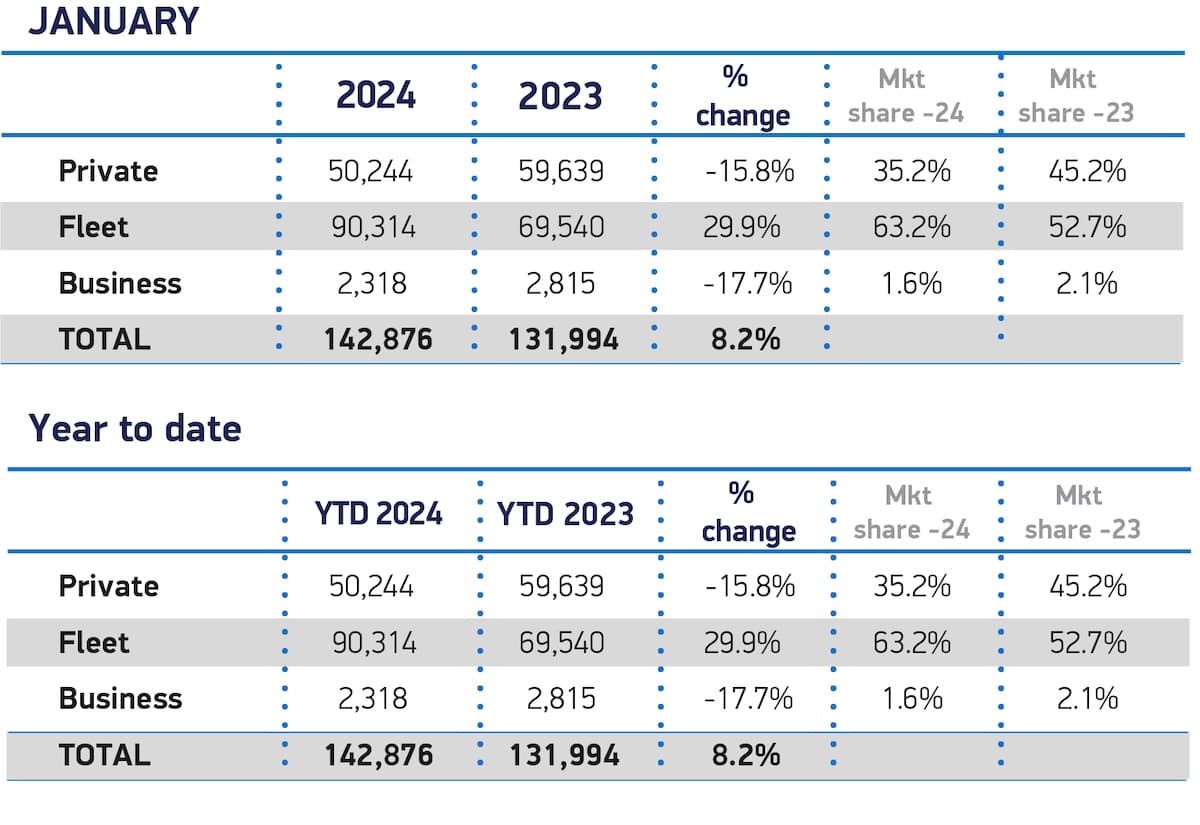

It was a very slow start to 2024 for private new car sales, recording the worst results in fifteen years according to data published this morning by the SMMT (Society of Motor Manufacturers and Traders).

Just over 50,000 new cars found their way into private hands in January, down 16% on the same month last year, which makes it the worst result since the early days of the great financial crisis in 2009. This is in stark contrast to fleet registrations, which were up 30% on last January. As a result, the overall market was up 8% compared the same month last year.

The January results are a continuation of sales trends from the second half of 2023, which saw private new car sales gradually slowing while fleet sales powered ahead to pre-pandemic levels.

Although there’s been a lot of media attention on poor EV sales to consumers, the fall in private new car sales is a much broader issue that covers all types of vehicles.

Private customers turning away from new cars

The last three months have seen private new car sales down 6% (November), 14% (December) and 16% (January). Looking longer term, the last six months of 2023 saw private sales down 2% compared to the same period in 2022, but the trend has been accelerating lately.

There’s no single reason for this, but rather a combination of factors. Car prices have been getting more and more expensive in recent years, even before the rapid increases in inflation and interest rates over the last year or so. Since since almost all new car buyers finance their cars in one way or another, that has pushed monthly payments upwards.

As a result, customers have been taking longer-term agreements, with four years now the norm rather than three years. Fewer customers appear to be changing their cars before the end of their agreements, preferring to wait until the last minute before swapping. As a result of customers keeping their cars longer, new car sales each year are falling.

This pattern has been further influenced by high inflation over the last year. Interest rates have been rising to combat inflation, providing a double-whammy on monthly car payments. Add in reduced levels of disposable income as other household bills eat into consumer salaries, and new cars have become unaffordable for more and more people.

There seems to be nothing on the horizon that’s likely to bring about dramatic change in these factors anytime soon, so we could be seeing a profound shift in the automotive industry.

Are we seeing the end of private new car ownership for all but the super-wealthy? That might sound overly dramatic, but private new car sales are down more than 35% compared to their peak in 2017, so maybe it’s not as silly as it sounds.

Poor consumer EV sales making things hard for car companies

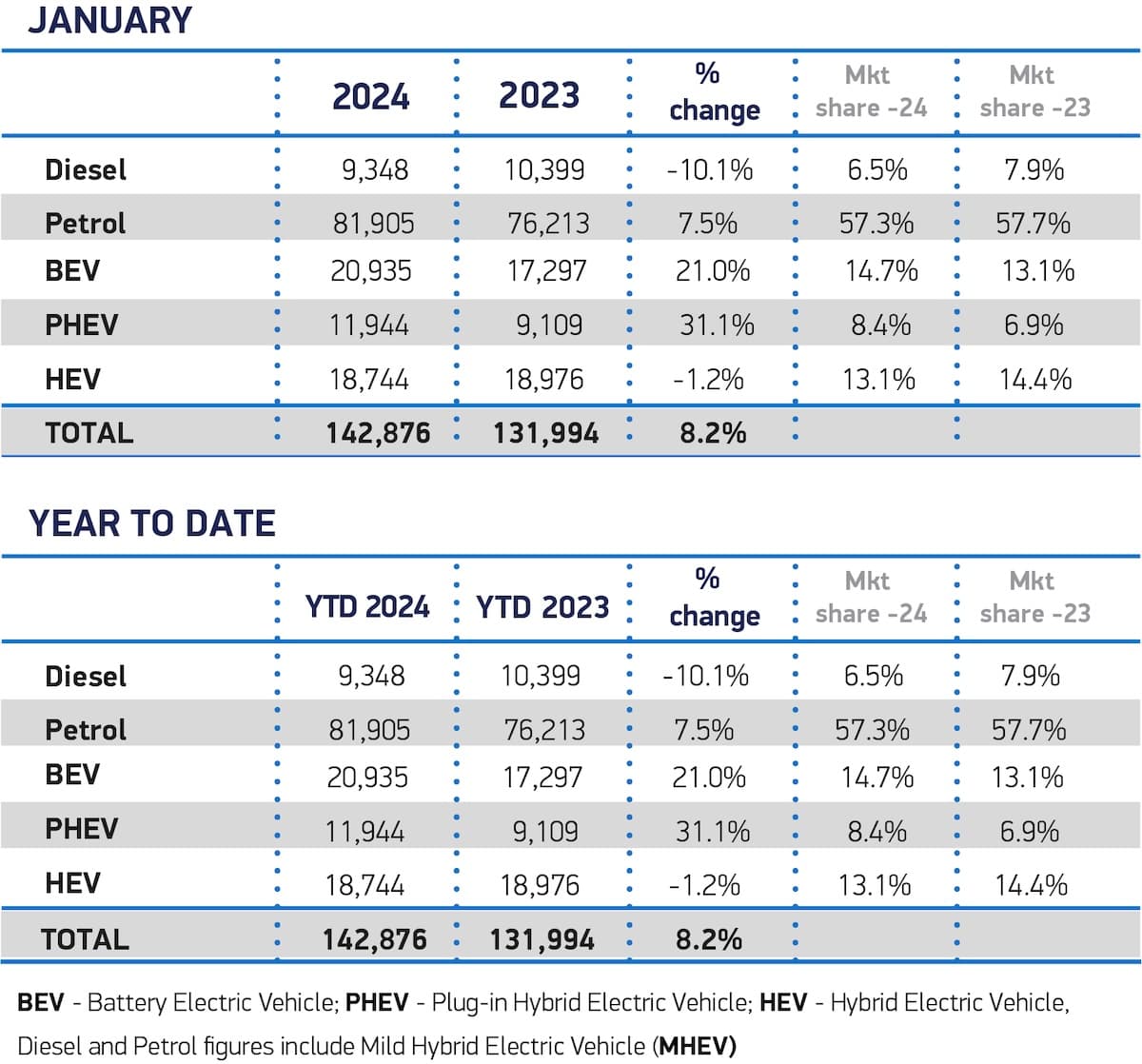

Having just said that poor consumer sales are more than just an EV problem, there’s no doubt that EV sales are making the problem worse. According to the SMMT, private new EV sales fell by 25% compared to last January, which is 9% worse than the overall fall in private new car sales. And this is the first month of the government’s new ZEV mandate coming into effect, which requires car companies’ total sales to be at least 22% EVs.

Overall, EVs took less than 15% of the new car market in January. That’s better than the same month last year, but a long way short of the 22% target. In fact, EV sales will have to increase by 50% on January’s numbers to hit that target.

The real demand may even be worse than that. We expect that at least some car manufacturers would have held over EV registrations from December to give them a small head start into the ZEV mandate for 2024. In addition, Tesla had a reasonable month, tripling its deliveries over last January. So many EV models from other brands have probably had a very poor month indeed.

Plug-in hybrids continued their mini-resurgence of recent months, while petrol continues to be the dominant fuel for new car sales. Regular hybrids had a surprisingly poor month, down 1% against overall market growth of 8%, while diesel was unsurprisingly poor.

In one small piece of good news, the SMMT has finally decided to stop listing mild hybrid petrol and diesel models separately from regular petrol and diesel models. That means we no longer have to make our own tables to put them back together again. Yay!

Good month, bad month

It’s been a mixed bag of results to start the year, with some brands performing well and others struggling. If you’re new to this, we rate a brand’s performance as ‘good’ if it outperforms the overall market by at least 10%. Given that the overall market was up 8%, that means a ‘good’ result means growth of at least 18% year-on-year.

Similarly, a ‘bad’ month means underachieving by at least 10% against the overall market. So for January, that means registrations falling by at least 2% compared to the same month last year.

It was a good month (at least 18% growth in registrations) for Abarth, Alpine, BMW, Cupra, GWM Ora, Jaguar, Jeep, Land Rover, Mini, Nissan, Peugeot, Renault, Smart, Subaru, Tesla and Vauxhall.

It was a bad month (a fall of at least 2%) for Audi, Bentley, Citroën, DS Automobiles, Fiat, Genesis, Lexus, Maserati, Mazda, MG, Polestar, Porsche, SEAT, Skoda, SsangYong (now called KGM), Toyota, Volkswagen and Volvo.

Therefore, these brands were more or less where you’d expect them to be: Alfa Romeo, Dacia, Ford, Honda, Hyundai, Kia, Mercedes-Benz and Suzuki.

Overall, Vauxhall had the largest growth in volume – up by more than 3,000 units – while Toyota saw the biggest fall (down by about 2,500 units).

As usual, Volkswagen was the country’s best-selling brand, ahead of BMW, Kia, Ford and Audi.

Kia Sportage tops the charts in January

The Kia Sportage pipped the Ford Puma (2023’s best-selling new car) to top the sales charts in January. The rest of the top ten consisted of familiar faces, although there were no Teslas to be seen. We’d expect to see the Model Y pop up in March, based on previous years.