As we have reported previously, the Bank of England has announced that it has opened an investigation into the UK car finance market, citing concerns over the state of the sector.

Predictably, the industry lobby groups and lapdogs leapt in to defend the status quo, claiming that everything is fine and warning of dire consequences for the UK car industry if the Bank interferes.

So why has the Bank of England chosen to open an investigation, and what is it looking for?

Part of an ongoing study of the UK credit market

The Bank of England has been monitoring credit and household debt for some time, which includes car finance along with house mortgages, credit cards, personal loans and so on. Unlike the Financial Conduct Authority, which has also opened its own investigation into the selling (and potential mis-selling) of car finance, the Bank of England is concentrating on the overall economic picture.

Car finance borrowing is growing at a much faster rate than the rest of the credit market and is now a £40 billion per year industry, with up to 90% of private new car sales now being financed by a personal contract purchase (PCP). This rapid growth has inevitably been spotted by the Bank, which would like to know more about how and why it is happening.

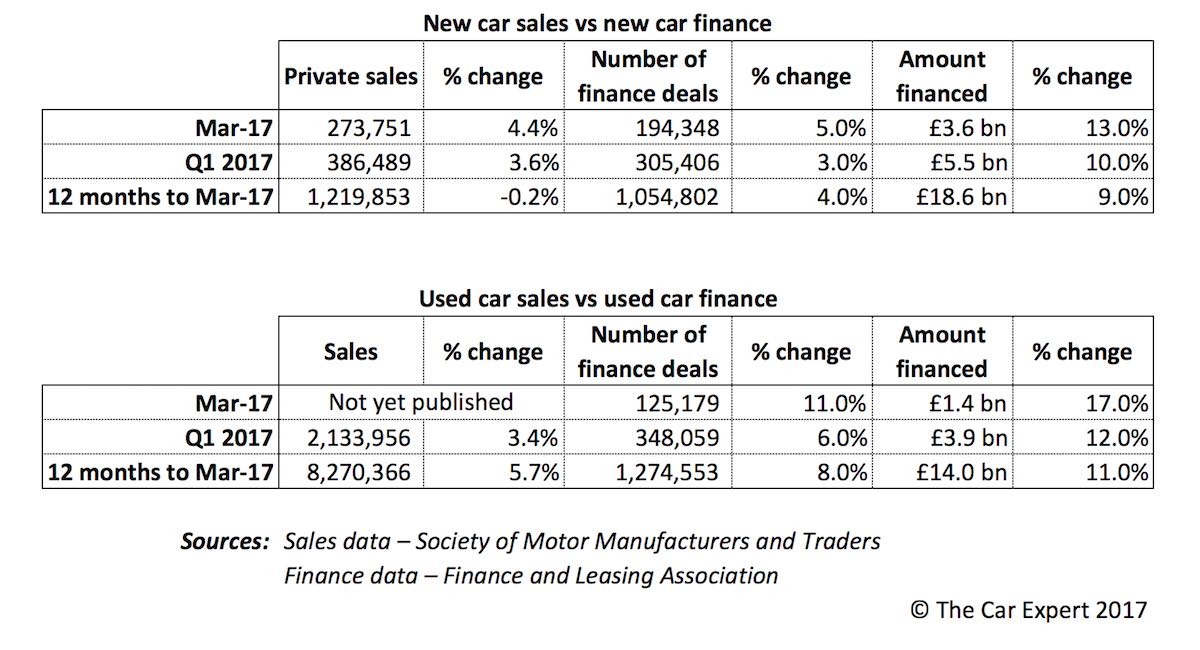

Last week, the Finance and Leasing Association published its results for the first quarter of 2017. These are shown below, along with data for private car sales over the same periods.

The results show that the number of new cars sold under finance has increased at much the same rate as the number of total sales, which is to be expected. However, the value of those loans has increased by 10%, meaning customers are borrowing more on each car. Over the last 12 months, this trend has been accelerating, with March 2017 alone showing a new car finance increase of 5% in terms of volume, but an increase of 13% by value.

For used cars, the pattern of customers taking out more finance and borrowing more per car is even clearer. Used car sales were up 3.4% on last year, but the number of loans increased by 6% and the amount financed increasing by 12%. Although the SMMT is yet to publish a month-by-month breakdown of used car sales for 2017, again we can see that the both the volume of finance deals and amount of money financed has been accelerating over the last 12 months.

Particular growth in sub-prime car finance sector

The Bank of England is also concerned that much of that growth is coming from ‘sub-prime’ customers, potentially leading to a lot of money being owed by high-risk borrowers. Closely connected to this is a concern that sub-prime customers are being loaned large amounts of money on highly unfavourable terms (ie – much higher interest rates and fees), further increasing the likelihood of these customers defaulting on their loans.

The Bank is concerned that any downturn in economic conditions could lead to large-scale defaulting on these finance deals, which would be bad news for both borrowers and lenders. It has been suggested that the Bank may impose tougher lending criteria to limit the amount of money being lent to higher-risk customers.

The industry has predictably reacted with outrage and warnings of catastrophe if lending criteria are tightened up.

Currently, high interest rates for sub-prime borrowers mean that such a customer could be paying the same per month as a regular ‘prime’ customer, but is only able to afford a cheaper car because much more of the monthly payment is simply interest.

So for £200/month on a PCP, a regular customer might be able to afford a £20,000 car. But for a sub-prime customer paying much more interest, their £200/month might only get them a £15,000 car.

The finance companies try to justify charging higher interest rates because the sub-prime borrower is considered a higher risk, but the combination of higher interest with generous borrowing limits simply makes a customer default more likely.

Are tougher affordability rules the answer?

If the lending criteria were made tougher, and the finance companies were not allowed to pile on the interest, then the sub-prime customer might still only be allowed to borrow enough money for a £15,000 car. But their monthly payments might now only be £150 per month instead of £200, which means they are less likely to default on that loan if they hit any financial trouble.

From the car industry’s point of view, they have still bought the same car, but the finance company is making a more normal profit margin on the deal, rather than milking those customers who can least afford it.

If the sub-prime customer does still default on a smaller loan with a lower interest rate, then at least the loan settlement figure is going to be lower. This gives them a better chance of being able to sell the car and settle all or most of their debt, rather than having an enormous debt still outstanding that could be far more damaging for a much longer time.

- Is the sky really about to fall in for PCP car finance?

- PCP car finance debate highlights widespread media confusion