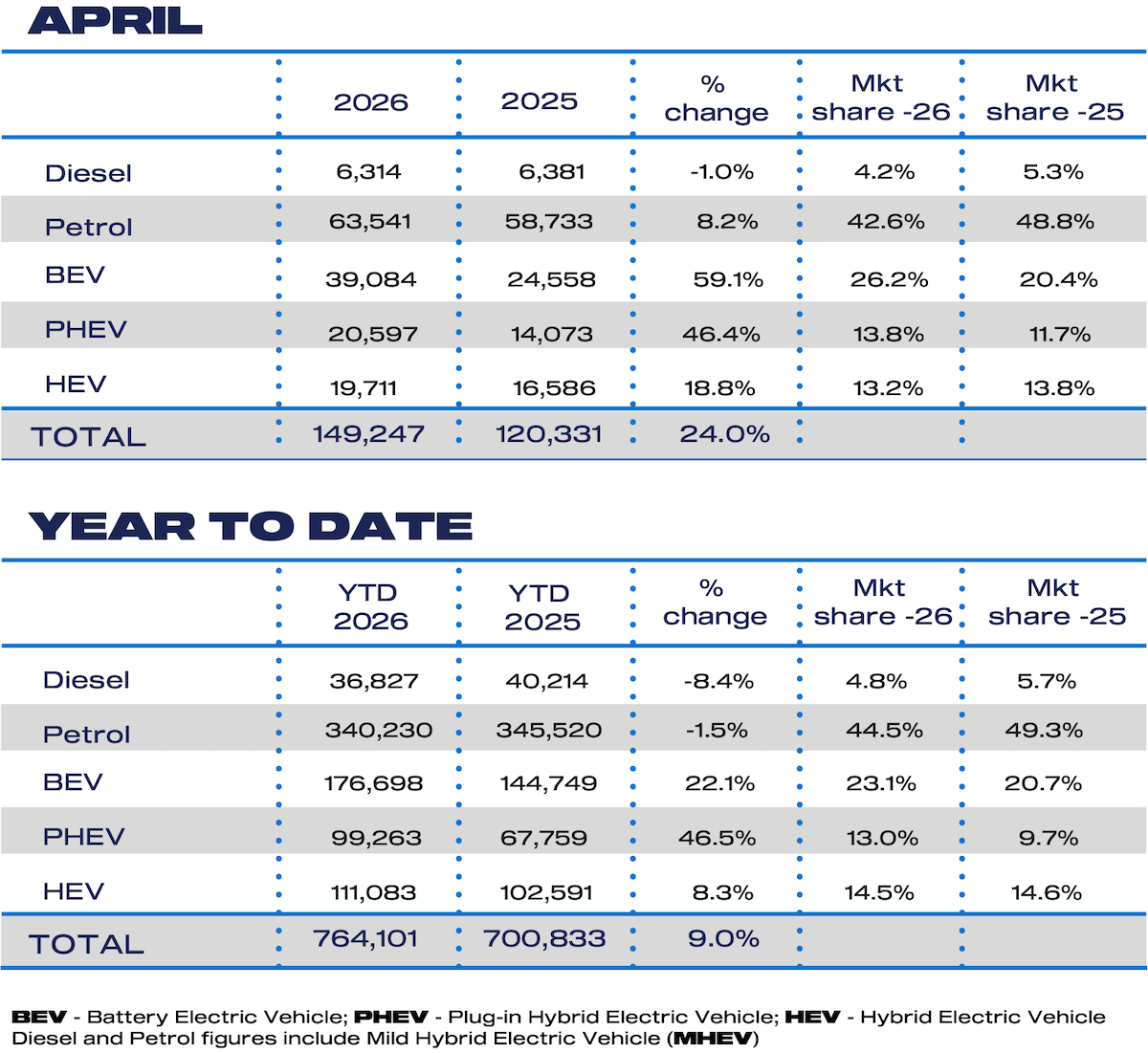

Electric car registrations grew by 60% in April compared to the same month last year, as demand skyrocketed in the face of ever-increasing fuel prices.

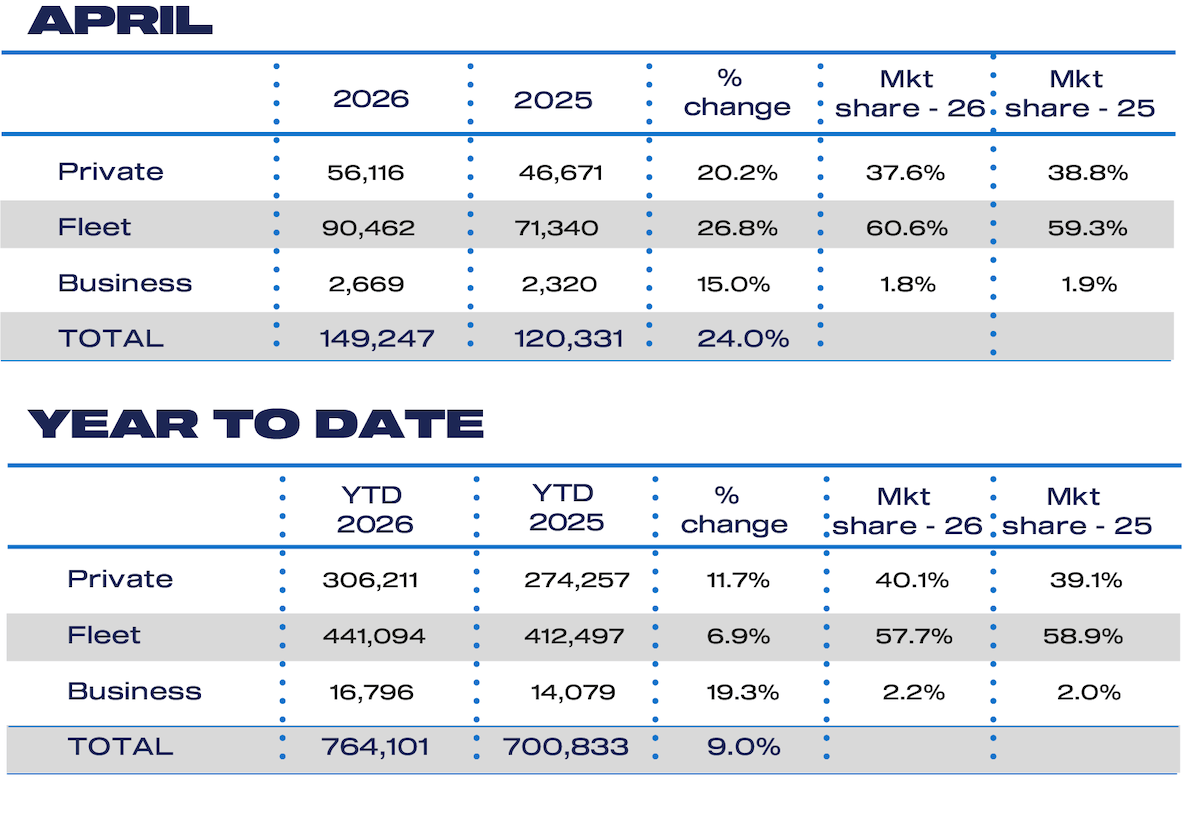

According to numbers published this morning by the Society of Motor Manufacturers and Traders (SMMT), the overall car market grew by 24% over last April, with strong growth from both private and fleet customers. But it was only EVs and plug-in hybrids that grew their market share, with petrol, diesel and basic (no plug) hybrids losing ground.

The impressive overall numbers need to be tempered somewhat by noting that last April was a particularly poor month, down 10% on the year before, so things weren’t quite as dramatic as they seemed.

Sky-high petrol prices fuelling EV demand

Not long after Donald Trump decided to invade Iran and send oil prices skyrocketing, we wrote that this oil crisis could be a catalyst for driving more customers to switch from fossil-fuel cars to EVs. We’re only two months into the war, with potentially months of petrol pricing pain still to come, but March and April have both seen sharp increases in new EV sales.

Combined with other industry data, like used EV sales and dealer time-to-sell information, and it’s clear that customers want EVs right now. Whether this shift continues or recedes once oil prices eventually come back down remains to be seen, but the longer the current situation in the Middle East drags on, the more likely it is that we will see permanent changes in customer car-buying behaviour.

This is also benefiting the sales of plug-in hybrids, particularly those that offer plenty of battery range. In what we believe to be a first, plug-in hybrids saw more registrations than standard (no plug) hybrids.

Good month, bad month

Even with an overall market growth of 24%, it wasn’t good news for all car brands in April.

It was a good month for Abarth, Alpine, BYD, Chevrolet, Citroën, Cupra, Fiat, Genesis, Jaecoo, Leapmotor, Lotus, Maserati, MG, Mini, Omoda, Skywell, Smart, Tesla and Xpeng. All of these brands outperformed the overall market by at least 10% – and this list includes about ten brands that make all or most of their cars in China.

Meanwhile, things weren’t so rosy for Alfa Romeo, Audi, BMW, Dacia, DS Automobiles, GWM, Honda, Hyundai, Ineos, Jeep, Kia, Land Rover, Lexus, Mazda, Nissan, Peugeot, Polestar, Renault, SEAT, Škoda, Subaru, Toyota and Volkswagen. All of these brands underachieved against the overall market by at least 10%

That meant that the following brands were about where we’d expect them to be: Ford, KGM, Mercedes-Benz, Porsche, Suzuki, Vauxhall and Volvo. These brands were within +/-10% of the overall market result.

Volkswagen remained the UK’s best-selling car brand, as usual, comfortably clear of Kia, BMW, Ford and Audi. However, if you include Chery Group’s three brands – Chery, Jaecoo and Omoda – under one umbrella (since they essentially operate as one brand for the moment), it would place second on the list.

MG had the largest absolute increase in sales volume, more than 3,000 cars up on the same month last year. Going in the other direction, SEAT sold 1,000 fewer cars – down 57% in a market that was up 24%.

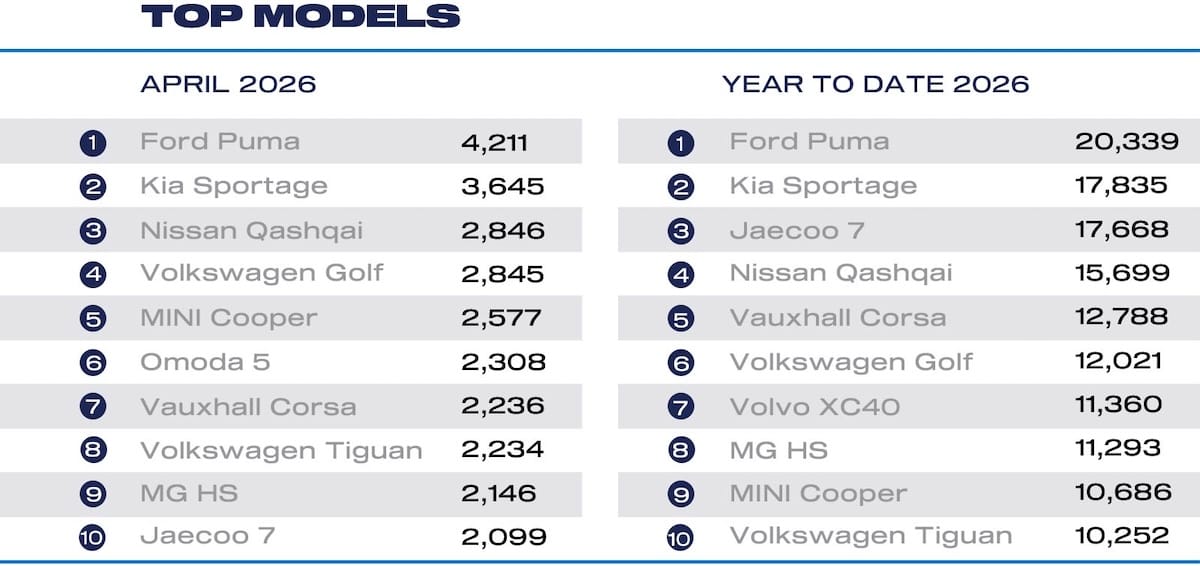

Puma back on top and extending its lead

The Ford Puma was back atop the sales charts in April, after being deposed by the Jaecoo 7 in March. That means it continues to edge away from its usual sales sparring partner, the Kia Sportage.

Last month’s star performer, the Jaecoo 7, slid back to tenth place in April, which also meant it slipped back to third place in year-to-date registrations. Its smaller cousin, the Omoda 5, popped up in sixth place, marking its first appearance in the top ten.

We’ll have our usual look at the top ten in coming days.